Labor & Economy

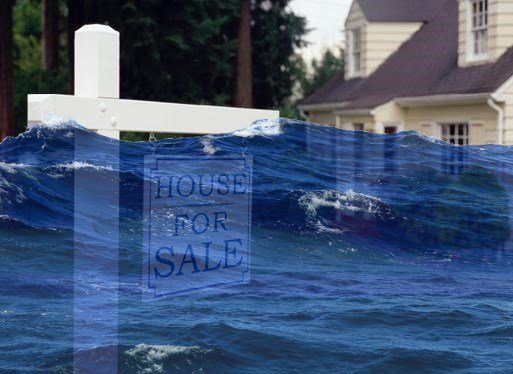

American Homeowners’ Underwater World

The release of former Treasury Secretary Tim Geithner’s new book, Stress Test — his self-serving account of the Obama administration’s effort to address the nation’s economic crisis and mortgage meltdown — has triggered a great deal of controversy and debate. Was the Obama economic team too cozy with, or too sympathetic, to Wall Street? Was the stimulus package large enough? Did Geithner, Larry Summers and Ben Bernanke stifle the views of dissidents within the administration — especially Council of Economic Advisors chair Christina Romer and FDIC chair Sheila Bair (perhaps not surprisingly, both women) — who urged bolder approaches?

But on at least one issue, there is a growing consensus: The Obama administration did too little, too late, to help troubled homeowners, who faced plummeting home prices and the risk of foreclosure.

Obama’s closest advisors wrongly assumed that as the economy improved, Americans would be better able to buy homes and pay the mortgage on existing homes. But the economic recovery was slower than expected, many unemployed people who did find jobs had to settle for less pay than before, and many homeowners found themselves with ballooning mortgage payments or with mortgages worth less than the value of their homes. Between 2006 and 2011, Americans lost about $7 trillion in home equity due to plunging housing prices — the largest overall loss of wealth than at any time since the Depression.

In a new book entitled House of Debt, and in a recent Washington Post column, economists Atif Mian of Princeton and Amir Sufi of the University of Chicago persuasively argue that the Obama administrative was too focused on bailing out banks and not focused enough on helping homeowners reduce their escalating mortgage debt. In his recent profile of Mian and Sufi, New York Times reporter Binyamin Appelbaum quoted Romer, now back at her teaching post at U.C. Berkeley, saying: “I now think that fiscal stimulus would have been more effective had we also had a more effective housing plan.” In back-to-back columns this week, New York Times columnists Paul Krugman (“Springtime for Bankers”) and Joseph Nocera (“Bankrupt Housing Policy“), echoed this view. Many others, including members of Congress, have joined this growing chorus.

But it is not too late for the Obama administration to act on this rare policy consensus. The key player on this issue is Mel Watt, the head of the powerful Federal Housing Finance Agency, which oversees Fannie Mae and Freddie Mac. Last week, Watt — who assumed his job in January — broke his silence at a speech at the Brookings Institution. It was his first major policy address and many people — bankers, developers, housing activists, mayors, members of Congress — eagerly awaited his remarks.

There are many things Watt can do to change the direction of these two mortgage giants which were put into government trusteeship after the mortgage meltdown. The eyes of many observers are on a variety of plans to restructure or privatize them. But one of the most pressing issues right now is the nation’s epidemic of “underwater” mortgages.

Many housing activists and homeowners hoped that Watt would announce his support for “principal reduction” — allowing Fannie and Freddie to re-set mortgages for underwater homeowners so that their payments reflect the current market value of their homes. This approach is already part of other mortgage modification programs. Experience reveals that it leads to more sustainable mortgages and reduces the likelihood of foreclosures. Moreover, Watt can do this without Congressional approval.

Unfortunately, Watt had little to say about the millions of Americans who are drowning in mortgage debt in his prepared remarks at Brookings. But in response to a question, he said: “It doesn’t mean we are not considering it. It just means we’re not ready to talk about it at this point,” according to the Los Angeles Times.

Some pundits and politicians claim that America’s housing market is now recovering from plummeting home prices and a years-long lull in new construction. But the so-called recovery is very uneven. Many communities remain devastated by widespread foreclosures and vacant homes. They will not be rescued by the rising tide of home prices, which has bypassed many parts of the country.

Many foreclosed houses in the hardest-hit areas are being purchased by Wall Street hedge funds and private equity firms, not homeowners who intend to live there. One of them, the Blackstone Group, is now the nation’s largest owner of single-family rental homes. These practices have artificially boosted home prices in some areas but made local housing markets even more volatile. The investors are making a killing renting the properties, but continuing to drain wealth from these communities.

It begs the question: recovery for whom?

Certainly not Jaime and Juana Coronel, whom Fannie Mae is trying to oust from their 1,200-square-foot home where they’ve lived for 25 years. The Coronels worked their entire lives, in landscaping and factory work, to afford the home where they raised their four kids. In 2010, after Jaime’s hours were cut at work, Fannie Mae foreclosed on them even though they had the income to qualify for a loan modification.

Since the foreclosure, Jaime (who recently suffered a stroke) and Juana have paid the equivalent of a modified mortgage payment in rent to Fannie Mae in order to continue living in their home. But last November, without giving a reason, Fannie Mae began eviction proceedings against the family. Jaime and Juana offered to repurchase their home at its current market value, about $200,000, which is what Fannie Mae would get for the house in the open market. Fannie Mae responded by demanding that they pay $400,000 — about twice the home’s market value — including a $45,000 cash deposit. A real estate agent from Century 21 verified that the Coronels qualify for a loan at the home’s current market value.

Joining forces with the community organizing group the Alliance of Californians for Community Empowerment (ACCE), the Coronels, along with friends and neighbors, have told Fannie Mae that they won’t move without a fight. They’ve demanded to know why Fannie Mae would put them out in order to sell it to someone else, most likely an investor, at a lower price.

The prolonged negotiations came to a head in a recent phone call between the Coronels and several Fannie Mae officials, including vice president Elonda Crockett. A Fannie Mae attorney told the Coronels that Fannie Mae is not allowed to sell them back the property at market value while they are still in the house. They even defended Fannie Mae’s current policy of opposing principal reduction, warning that it would lead to an epidemic of families refusing to pay their mortgages — despite a lack of evidence that anything of the sort happened when banks reduced principal on many loans as part of mortgage settlements.

The Coronels are hardly alone. The total value of America’s owner-occupied housing remains $3.2 trillion below 2006 levels. According to Zillow, a real estate database, 9.8 million households still owe more on their mortgages than the market value of their homes. That’s one-fifth of all mortgaged homes. Without government intervention, many of them are at risk of joining the almost five million households that have already suffered through foreclosure since the housing bubble burst in 2007.

With my coauthors Alex Schwartz of the New School, Gregory Squires of George Washington University, Saqib Bhatti of the Nathan Cummings Foundation, and Rob Call of MIT, I conducted a study, Underwater America: How the So-Called Housing Recovery is Bypassing Many American Communities, which was released last week by the Haas Institute at UC-Berkeley. Our study identified the 15 metropolitan areas, 100 cities, and 395 ZIP codes with the highest proportion of underwater mortgages.

How bad is it? More than 10 million Americans, spread across 23 states, live in ZIP codes where between 43 percent and 76 percent of homeowners are under water. The biggest concentrations are in Georgia, Florida, Illinois, Michigan and Ohio. Places with so many underwater homes are toxic; they depress the value of surrounding homes and undermine local governments’ fiscal health.

The blame for this tragedy lies mostly with banks’ risky, reckless and sometimes illegal lending practices. In the late 1990s and early 2000s, millions of Americans bought or refinanced homes in an overheated market. Mortgage brokers lied or misled borrowers about the terms of these mortgages, often pushing borrowers into high-interest subprime loans, even when they were eligible for conventional mortgages.

They particularly targeted minority areas. In 2006, when subprime lending was at its peak, 54 percent of blacks, 47 percent of Latinos and 18 percent of whites received high-priced loans, according to the Federal Reserve Board.

Not surprisingly, the nation’s worst underwater areas are disproportionately in black and Latino neighborhoods. In almost two-thirds of the hardest-hit ZIP codes, African-Americans and Latinos account for at least half of the residents.

The banks’ risky loans eventually came crashing down, devastating communities and causing financial havoc. The federal government rescued the banks, but nobody came to the rescue of the homeowners and communities the banks left behind.

The banks own some of these underwater loans, but when homeowners ask them to reset mortgages, they often get a cold shoulder or a bureaucratic run-around. In 2012, some of the biggest banks signed a settlement agreement with 49 state attorneys general to modify mortgages. This has resulted in some mortgage modifications, but many of these banks continue to heap abuse on their customers, and sufficient relief has not reached trapped homeowners. As Mian and Sufi point out in House of Debt, the Obama administration created several initiatives to help troubled borrowers, but these programs do not require banks to reset loans as a condition of getting federal funds. The government’s Home Affordable Modification Program (HAMP) has helped only one-quarter of the four million homeowners it was supposed to reach.

Many banks and private mortgage companies pooled large numbers of subprime loans into private securities and sold them to investors. The banks that service these securities have used principal reduction on some loans but, in general, they’ve been reluctant to do so, which will eventually push many homeowners over the cliff into foreclosure.

In the face of the financial industry’s intransigence and the federal government’s half-hearted measures, many local officials have their backs are against the wall. Some are prepared to address the problem of underwater mortgages by using their eminent domain authority to purchase these troubled loans from lenders and re-sell them to homeowners at current market values.

Richmond, California is the first city to adopt this idea, but the approach is gaining credibility as local officials confront the ravages of underwater mortgages in their communities. In the next few months, a growing number of cities are likely to embrace the eminent domain solution. The banking and securities industry is clearly worried about this growing movement. They’ve organized a webinar this week, sponsored by the American College of Real Estate Lawyers, to encourage corporate lawyers to challenge local governments trying to help underwater homeowners.

Local activists and city officials are still hoping that the Obama administration — and particularly Mr. Watt — will take action. The most important thing they can do is get Fannie Mae and Freddie Mac to adopt principal reduction.

Fannie and Freddie own and/or guarantee the biggest bulk of the nation’s underwater loans. Watt’s predecessor as FHFA head — Ed DeMarco, a holdover Bush appointee — opposed government efforts to help homeowners hurt by the Wall Street mortgage meltdown and the dramatic plunge in housing values. But in January, Congress finally confirmed Watt after a seven-month delay orchestrated by Congressional Republicans.

Although not well-known to the general public, FHFA controls over $5 trillion in housing assets and has enormous influence over the nation’s mortgage market, including the lending practices of banks.

Watt should allow, encourage, and even require banks to modify mortgages for “underwater” homeowners (with loans controlled by Fannie and Freddie) so they can stay in their homes and pay their mortgages based on the current value of their home. If underwater mortgages were reset to fair-market values of homes, it would help homeowners and communities alike, and pump billions of dollars into the economy each year. It would also save taxpayers huge sums, especially local governments that have lost property tax revenues but still have to pay for the maintenance and security of vacant properties.

In addition, Watt should:

- Allow renters to remain, and continue to pay rent, in foreclosed homes with leases, fair rents, just cause/no fault eviction and quality conditions.

- Comply with federal law that requires Fannie Mae and Freddie Mac to contribute a percentage of their (now substantial) profits to the National Housing Trust Fund to help build, rehabilitate and preserve affordable housing

- Make it a priority to sell foreclosed Fannie and Freddie homes to residents and nonprofits rather than absentee investors.

- Issue a statement nullifying DeMarco’s threat to retaliate against homeowners within any jurisdiction that dared to use its eminent domain authority to purchase underwater mortgages.

- Restore Fannie and Freddie’s role in investing in rental housing, which DeMarco scaled back over the past two years without any explanation, even though their rental investments remained profitable throughout the crisis.

Watt fills the FHFA job at a time when the public opinion is increasingly concerned with widening inequality, a declining standard of living, and the growing political influence of big business and Wall Street.

Watt can’t fix all these problems by himself. But he has more power than any other single person to stem the ongoing damage of the mortgage crisis by enacting a long-awaited program of principal reduction — a win/win deal with American homeowners and communities.

What is Watt waiting for?

Critical Audit of California’s Efforts to Reduce Homelessness Has Silver Linings

Despite Promises of Transparency, California Justice Department Keeps Probe into L.A. County Sheriff’s Department Under Wraps

The Mission to Save the World Through Regenerative Farming

On the Chopping Block: California’s Climate Program for Low-Income Housing

Climate + Young Voters = Biden Victory, Right? It’s More Complicated Than That.

Organizing the Slopes

Dispelling the Stereotypes About California’s Low-Wage Workers

The Transatlantic Battle to Stop Methane Gas Exports From South Texas

700,000 Undocumented Californians Recently Became Eligible for Medi-Cal. Many May Be Afraid to Sign Up.

Report: Banks Should Set Stricter Climate Goals for Agriculture Clients

Tried as an Adult at 16: California’s Laws Have Changed but Angelo Vasquez’s Sentence Has Not

Despite Promises of Transparency, California Justice Department Keeps Probe into L.A. County Sheriff’s Department Under Wraps

‘Every Day the Ocean Is Eating Away at the Land’

No, the New Minimum Wage Won’t Wreck the Fast Food Industry or the Economy

Critical Audit of California’s Efforts to Reduce Homelessness Has Silver Linings

Nurses Union Says State Watchdog Does Not Adequately Investigate Staffing Crisis

Economist Michael Reich on Why California Fast-Food Wages Can Rise Without Job Losses and Higher Prices

In Georgia, a Basic Income Program’s Success With Black Women Adds to Growing National Interest

Report: Banks Should Set Stricter Climate Goals for Agriculture Clients

Unionizing Planned Parenthood

CLASS WAR: The Temecula School Board Battle

Excavating the Future: Stopping AAPI Hate

Excavating the Future: Stopping AAPI Hate

Excavating the Future: Guarding the Hidden Archive

Excavating the Future: Breaking the Silence

Excavating the Future: Guarding the Hidden Archive

ILL HARVEST

Kaiser Therapists: Strike Is About Complying With the Law

‘What They Need Is Someone at Their Side’

Kaiser Therapists Say Patient Neglect Compels Them to Strike

-

Latest NewsApril 3, 2024

Latest NewsApril 3, 2024Tried as an Adult at 16: California’s Laws Have Changed but Angelo Vasquez’s Sentence Has Not

-

Latest NewsApril 17, 2024

Latest NewsApril 17, 2024Despite Promises of Transparency, California Justice Department Keeps Probe into L.A. County Sheriff’s Department Under Wraps

-

Latest NewsMarch 20, 2024

Latest NewsMarch 20, 2024‘Every Day the Ocean Is Eating Away at the Land’

-

State of InequalityApril 4, 2024

State of InequalityApril 4, 2024No, the New Minimum Wage Won’t Wreck the Fast Food Industry or the Economy

-

State of InequalityApril 18, 2024

State of InequalityApril 18, 2024Critical Audit of California’s Efforts to Reduce Homelessness Has Silver Linings

-

State of InequalityMarch 21, 2024

State of InequalityMarch 21, 2024Nurses Union Says State Watchdog Does Not Adequately Investigate Staffing Crisis

-

Latest NewsApril 5, 2024

Latest NewsApril 5, 2024Economist Michael Reich on Why California Fast-Food Wages Can Rise Without Job Losses and Higher Prices

-

Latest NewsMarch 22, 2024

Latest NewsMarch 22, 2024In Georgia, a Basic Income Program’s Success With Black Women Adds to Growing National Interest